Buying a home has become extremely difficult for many families in Pakistan. Property prices continue rising, rent increases every year, and saving enough money for ownership feels almost impossible for salaried and middle-income households. Because of this situation, many people are now paying close attention to the Wazir-e-Azam Apna Ghar Program 2026.

The program is designed to help low and middle-income families access housing finance with easier repayment options, longer loan tenure, and lower markup rates during the early years. For families who have spent years living in rented homes, this scheme may provide a realistic path toward home ownership if managed carefully and responsibly.

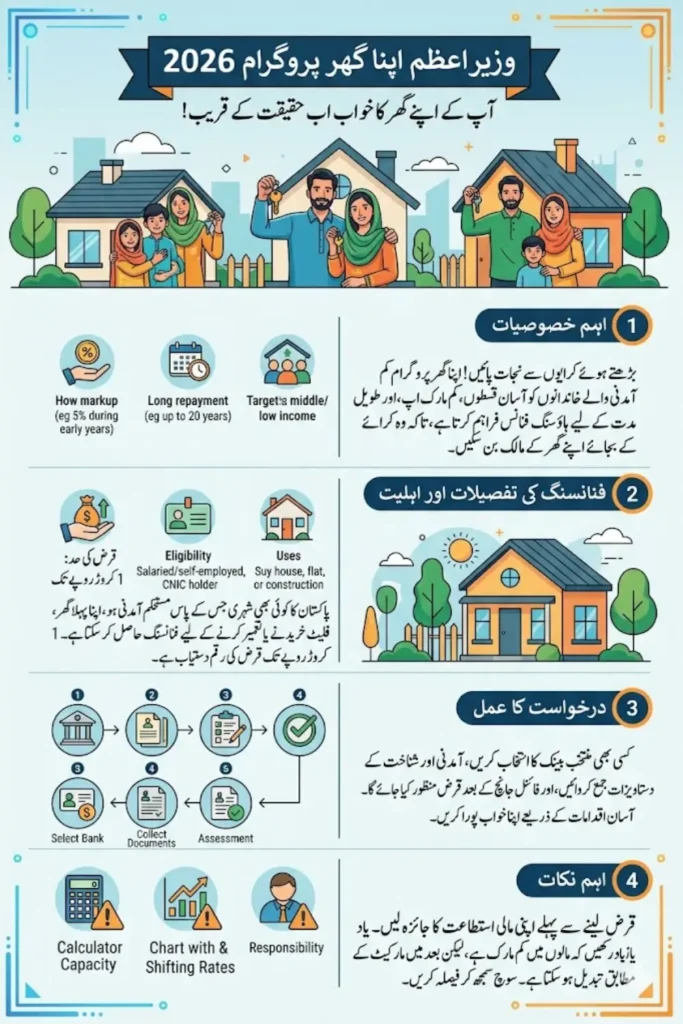

What Is the Wazir-e-Azam Apna Ghar Program?

The Wazir-e-Azam Apna Ghar Program 2026 is a government-supported housing finance initiative introduced to help eligible Pakistani citizens build, buy, or complete their own homes through subsidized financing. The scheme mainly targets families that cannot easily afford traditional bank loans because of high interest rates and short repayment periods.

Under this program, approved applicants can apply for financing through participating banks and housing finance institutions. The goal is to reduce financial pressure by offering affordable repayment plans and easier access to home financing compared to regular commercial property loans.

Why This Program Matters for Ordinary Families

Many families in Pakistan spend decades paying rent without building any personal asset. In major cities, monthly rent can already be equal to or even higher than a home financing installment. That is one of the main reasons why housing schemes like Apna Ghar are attracting attention.

Here is why many applicants are considering the program seriously:

| Renting a Home | Home Financing |

|---|---|

| Rent increases frequently | Installments are more predictable |

| No ownership benefit | Long-term property ownership |

| Frequent house shifting | Stable family environment |

| No asset creation | Property investment opportunity |

| Advance rent pressure | Structured repayment plan |

For families with stable income, financing may become a better long-term option than continuously paying rising rental expenses.

Loan Amount Available Under the Scheme

One of the biggest highlights of the Apna Ghar Program is the financing limit available to eligible applicants. Under the scheme, applicants may apply for housing loans up to Rs. 10 Million depending on income level, repayment capacity, and property verification.

The financing can generally be used for:

- Buying a small house

- Purchasing approved flats or apartments

- Constructing a house on owned land

- Completing partially built homes

- Building modest residential properties

However, applicants should understand that approval for the full amount is not guaranteed. Banks still review income stability, existing liabilities, credit history, and repayment ability before final approval.

You can also read: E-Learn She Earn 2026 Punjab

Installment Structure and Markup Rates Explained

One of the biggest reasons this scheme is receiving public attention is the subsidized markup structure during the initial years. The government aims to make early installments more manageable for low and middle-income households.

First Phase of Financing

During the first 10 years, the expected markup rate may remain around 5% under subsidized financing conditions. This lower rate can significantly reduce the monthly financial burden compared to normal bank loans.

Remaining Financing Period

After the subsidized period ends, the financing may shift toward market-based banking rates depending on the policy framework at that time. Applicants should understand this carefully before making long-term financial commitments.

Many people focus only on the low initial rate while ignoring future repayment adjustments. Understanding the complete financing structure is extremely important before applying.

Why Lower Initial Installments Matter

For middle-class households, the early years of financing are usually the most financially sensitive period. Families already manage multiple monthly expenses, and large installments can quickly become difficult to handle.

Common household expenses include:

- School and college fees

- Utility bills

- Grocery inflation

- Transportation costs

- Medical expenses

- Family support responsibilities

Lower initial installments may help families transition from rent toward ownership more comfortably without creating immediate financial pressure.

Property Size Limits Under the Program

The Apna Ghar Program mainly focuses on affordable residential housing instead of luxury property investments. Because of this, certain property size limits are expected to apply under the financing rules.

| Property Type | Expected Size Limit |

|---|---|

| Residential House Plot | Up to 10 Marla |

| Apartments / Flats | Approved modest size |

| Luxury Housing | Usually not prioritized |

These restrictions help ensure that financing benefits genuine residential applicants instead of high-value commercial investors.

Who Can Apply for the Apna Ghar Program?

The scheme mainly targets first-time homeowners and middle-income Pakistani families. While exact conditions may vary slightly between banks, several basic requirements are expected across most applications.

Basic eligibility may include:

- Pakistani citizen

- Valid CNIC or NICOP

- Stable monthly income

- Satisfactory repayment capacity

- Property verification compliance

- First-home preference in many cases

Both salaried and self-employed individuals may qualify if they can provide proper income proof and banking records.

Required Documents for Application

Incomplete documentation is one of the most common reasons housing applications face delays. Applicants should prepare all financial and identity records before starting the process.

Commonly required documents include:

- Original CNIC

- Salary slips or income proof

- Bank statements

- Property ownership documents

- Utility bills

- Employment verification letter

- Tax documents if applicable

- Business proof for self-employed applicants

Banks may request additional documents depending on the property type and financing amount.

Step-by-Step Application Process

The financing process is expected to operate through approved banks and housing finance institutions connected with the government scheme. Understanding the process early can help applicants avoid confusion later.

Step 1 – Select a Participating Bank

Applicants first choose a partner bank offering Apna Ghar financing facilities.

Step 2 – Submit Required Documents

The bank begins reviewing identity, income, employment, and property-related paperwork.

Step 3 – Financial Assessment

The institution evaluates:

- Monthly income

- Existing loans

- Debt-to-income ratio

- Credit history

- Repayment ability

Step 4 – Property Verification

Legal verification of the property may also be conducted before approval.

Step 5 – Loan Approval and Disbursement

If approved, financing may be released in phases for construction cases or directly for approved purchases.

Expected Monthly Installment Examples

Monthly installments can vary significantly depending on loan amount, tenure, and markup structure. Applicants should always calculate repayments carefully before making commitments.

Here is a simplified example for understanding only:

| Loan Amount | Estimated Tenure | Approximate Early Installment |

|---|---|---|

| Rs. 3 Million | 20 Years | Lower monthly burden |

| Rs. 5 Million | 20 Years | Moderate installment |

| Rs. 10 Million | 20 Years | Higher repayment pressure |

Actual installments may differ depending on bank policy, markup changes, insurance, and processing charges.

Common Mistakes Applicants Should Avoid

Many people become excited about low markup financing but ignore long-term financial planning. This often creates repayment stress later.

Some common mistakes include:

- Choosing property beyond budget

- Ignoring future markup adjustments

- Underestimating household expenses

- Applying with incomplete documents

- Taking maximum loan unnecessarily

- Not understanding bank terms carefully

A smaller affordable home is often financially safer than taking a very large loan that becomes difficult to manage.

Benefits and Challenges of Housing Financing

Housing finance can create long-term stability, but it also comes with responsibilities that applicants should understand clearly before signing any agreement.

Major Benefits

- Home ownership opportunity

- Asset creation over time

- Reduced dependence on rental housing

- Long repayment period

- Lower early financing cost

Possible Challenges

- Long-term financial commitment

- Future markup adjustments

- Late payment penalties

- Property verification complications

- Processing and registration expenses

Careful financial planning remains the most important factor for successful repayment.

Can Overseas Pakistanis Apply?

Some overseas Pakistanis may also qualify under the scheme if they hold valid NICOP documentation and meet income verification requirements. However, banks often apply stricter financial checks for overseas applicants because foreign income verification can be more complex.

Applicants working abroad may need additional documents such as overseas employment proof, remittance records, tax details, and verified banking history.

Will This Program Help Pakistan’s Housing Crisis?

Pakistan faces a serious housing shortage, especially for low and middle-income families. While one scheme alone cannot fully solve the problem, programs like Apna Ghar can still provide meaningful support for families struggling with rising rent and expensive property markets.

If the financing process remains transparent, affordable, and properly regulated, the scheme may help thousands of families move toward home ownership who otherwise might never qualify for regular commercial housing loans.

FAQs

Can applicants buy flats under this scheme?

Yes, approved apartments and flats may qualify depending on financing rules and bank approval.

Is the 5% markup permanent for the entire loan?

No. The subsidized rate mainly applies during the early financing years before possible market-based adjustments later.

Can self-employed individuals apply?

Yes. Self-employed applicants may qualify if they provide proper income proof and banking documentation.

Is owned land necessary before applying?

Not always. Some financing options may include purchase plus construction depending on bank policy.

Can government employees apply?

Yes, eligible salaried government employees may apply if they meet repayment and verification conditions.

What is the repayment tenure?

The financing tenure may extend up to 20 years depending on the approved loan structure.

Conclusion

The Wazir-e-Azam Apna Ghar Program 2026 could become an important housing opportunity for middle and lower-income families searching for affordable home financing in Pakistan. With lower initial markup rates, longer repayment tenure, and government-backed support, the scheme offers a more practical alternative compared to traditional commercial financing for many households.

Still, applicants should avoid emotional decisions and calculate affordability realistically before applying. Choosing a manageable loan amount, understanding future repayment conditions, and preparing proper documentation can make a major difference in long-term financial stability.